The SECURE 2.0 Act isn’t just a minor update – it’s a restructuring of how small businesses handle retirement benefits. If you’re running a business and want to retain employees, improve financial security, and maximize cash flow, here’s what actually matters.

In this article, we will summarize the SECURE 2.0 Act’s key provisions and how it affects small businesses, including:

- Enhanced Tax Credits for Small Businesses

- Mandatory 401k Auto-Enrollment

- Increased Catch-Up Contributions for Employees Aged 60-63

- Employer Matching for Student Loan Repayments

- Emergency Savings Accounts within 401(k) Plans

- Changes to Required Minimum Distribution (RMD) Rules

- Other notable provisions include adjustments to the 10-Year Rule for Inherited IRAs, introduction of Qualified Longevity Annuity Contracts (QLACs), and provisions for Roth SEP IRAs.

Let’s begin!

Bigger Tax Credits for Small Businesses

Most small businesses avoid offering retirement plans because of the cost. SECURE 2.0 eliminates that excuse.

- If you have 50 employees or fewer, you now get a 100% tax credit for startup costs – up to $5,000 per year for three years.

- An additional $1,000 per employee credit applies for employer contributions (phase-out for 51-100 employees).

This is free money to set up a 401(k), yet most business owners won’t take advantage of it because they assume it’s too complicated. It’s not. You just need the right structure.

401(k) Auto-Enrollment: No More Excuses

Starting in 2025, if you set up a new 401(k) or 403(b), employees must be automatically enrolled at 3% of their salary, increasing each year until reaching at least 10%, but no more than 15%.

- Auto-enrollment significantly increases participation. Employees who wouldn’t normally save for retirement now have a default plan in place, which is good for them and good for your business’s retention strategy.

- Businesses with 10 employees or fewer or those that have been in business for less than three years are exempt.

Catch-Up Contributions for Ages 60-63

If you’re in the final stretch before retirement, the government just gave you a major opportunity.

- Starting in 2025, if you’re between 60-63, your catch-up contribution limit jumps to $10,000 (or 150% of the standard limit, whichever is greater).

- If you’re at your highest earning years, this is one of the best ways to accelerate tax-free retirement savings.

Roth IRA Catch-Up Contributions

Catch-up contributions are getting a Roth treatment – and it’s not optional.

- If you earn over $145,000 per year, any catch-up contributions must be made to a Roth IRA account, meaning they’re taxed upfront but grow tax-free.

- This change applies to 401(k), 403(b), and 457(b) plans.

Matching Contributions for Student Loan Payments

Employees no longer need to contribute to their 401(k) to get a match.

- Starting in 2024, employers can match student loan payments as a retirement contribution.

- Example: If an employee pays $200 toward student loans, you can match that with $200 into their 401(k).

For small business owners competing for talent, this is a game-changer. If your competitors aren’t offering it, you should.

Emergency Savings Inside a 401(k)

401(k)s have always been hands-off money – until now.

- Employees can set up emergency savings within their 401(k) (up to $2,500).

- These funds stay liquid – they can withdraw them at any time without penalties.

This removes the number one reason employees don’t contribute – fear of not being able to access their cash.

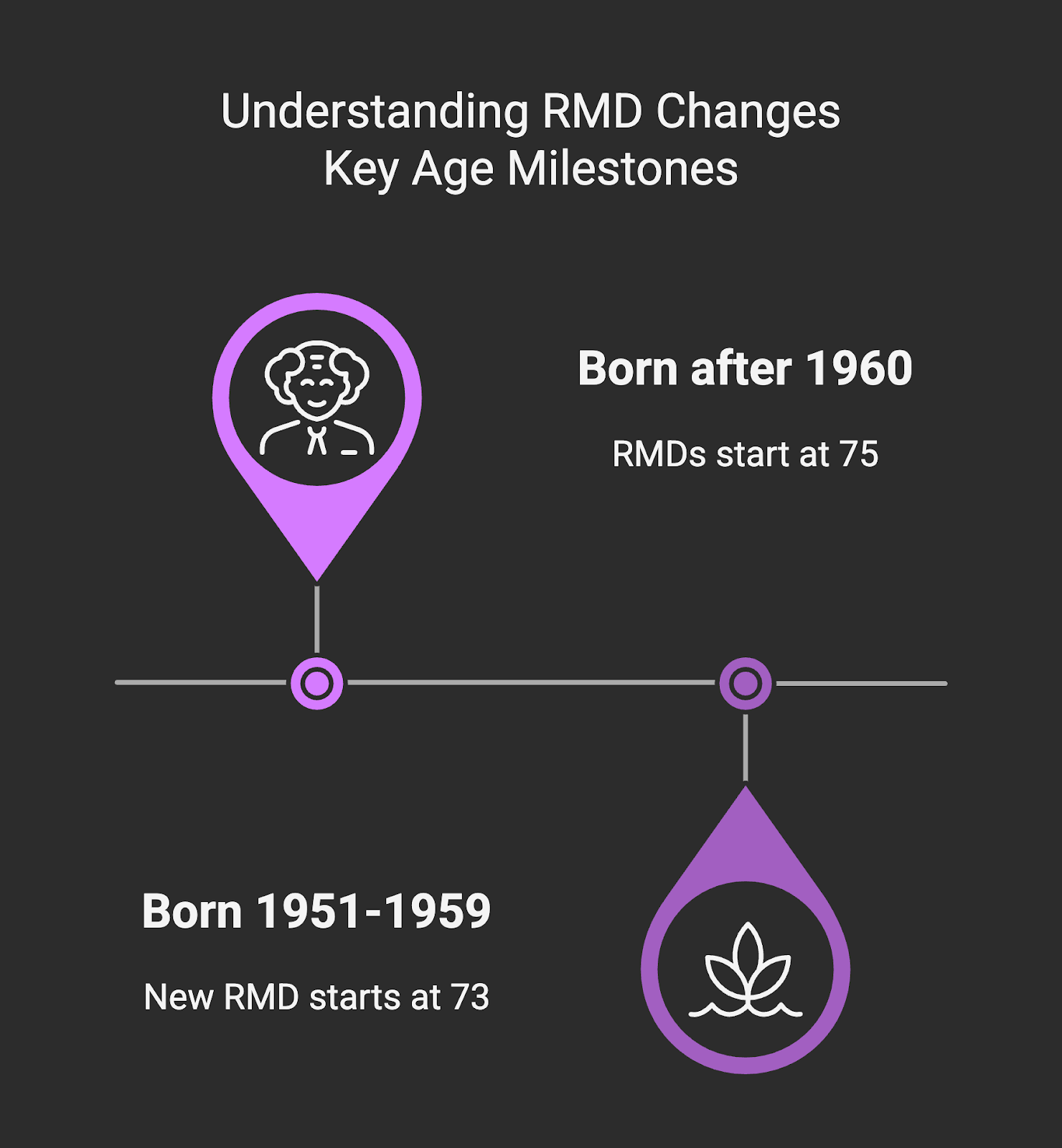

Required Minimum Distribution (RMD) Changes

If you don’t want to start taking money out of your retirement account too early, SECURE 2.0 gives you more time.

- New RMD age: If you were born between 1951 and 1959, RMDs start at age 73.

- If you were born in 1960 or later, RMDs start at age 75.

- Roth 401(k)s are now exempt from RMDs starting in 2024, aligning them with Roth IRAs.

10-Year Rule for Inherited IRAs

The IRS clarified that non-spouse beneficiaries of inherited IRAs must fully deplete the account within 10 years.

- If the original owner had started RMDs, beneficiaries must continue taking RMDs within that period.

Qualified Longevity Annuity Contracts (QLACs)

A QLAC is an annuity that lets you defer RMDs and guarantee income later in life. SECURE 2.0 increases the contribution limit for QLACs, making them a stronger retirement planning tool.

What This Means for You as a Business Owner

- If you don’t already offer a 401(k), the government is literally paying you to do it.

- If you already have a plan, auto-enrollment is coming – prepare now.

- If you want to attract top talent, matching student loans and emergency savings set you apart from competitors.

- If you’re in your final years before retirement, you now have a way to maximize tax-free savings.

Most business owners won’t make the right moves here. The ones that do will save a ton on taxes and keep employees longer.

Need a Plan That Actually Works?

Retirement plans and strategic finance aren’t separate – they should work together to maximize cash flow, profitability, and long-term scalability.

If you’re serious about building wealth and structuring your finances for growth, let’s build a plan tailored to your business.

Schedule a call today and let’s talk about how SECURE 2.0 impacts your bottom line.

Sources: