Form 5500-EZ: The $150,000 Mistake Hiding in Your Retirement Plan

Got a solo 401(k)?

Then the IRS is expecting a form from you. One you’ve probably never heard of.

It’s called Form 5500-EZ. It’s short, easy to overlook, and skipping it can cost you up to $150,000 in penalties.

Most business owners miss it. Their CPA doesn’t file it. Their plan provider doesn’t flag it. The IRS won’t remind you.

But when they catch it, they charge you.

If you’ve got money in a one-participant retirement plan and no one’s tracking this form, you’re exposed. Here’s what to do about it.

The Three Types of Form 5500: Know Which One You Need

Not all Form 5500 filings are the same. There are three variations, and choosing the wrong one or ignoring the one that applies to you can lead to compliance issues or steep penalties. If your business is a sole proprietorship, you may need to obtain a business EIN rather than using your SSN, as the IRS requires the correct identification for Solo 401(k) plan filings.

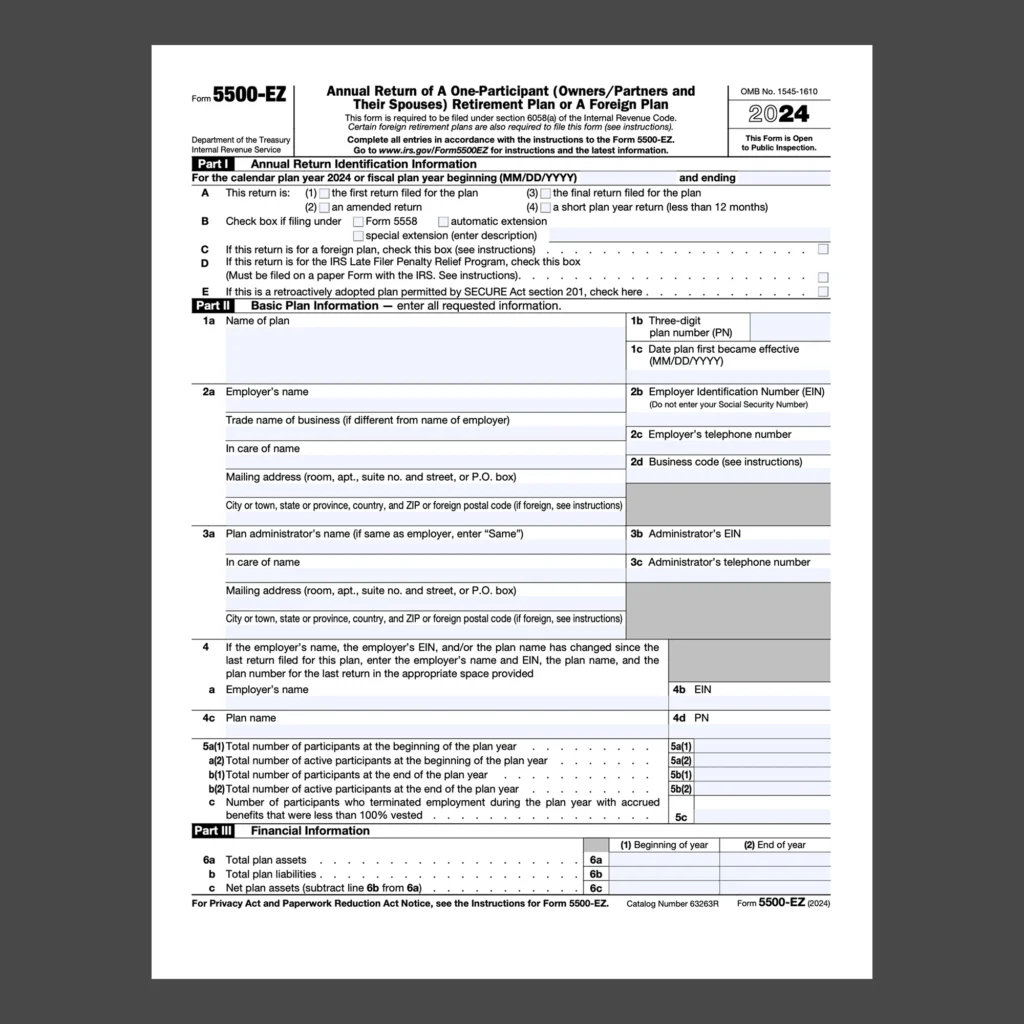

When completing Form 5500-EZ, you will need to provide your business code and business EIN, which are essential for proper IRS classification and identification. You must also include the plan number, especially if you have restated, updated, or transferred your Solo 401(k) plan, to ensure accurate IRS tracking and compliance. Be sure to list your business EIN on line 2b of Part II of Form 5500-EZ.

1. Form 5500-EZ

Applies to one-participant retirement plans. This typically covers solo 401(k)s, which are a type of defined contribution plan offering flexibility in contributions and no minimum funding requirement, or owner-only defined benefit plans. If it’s just you or you and your spouse, this is the form you need. If you adopted a pre-approved plan, be sure to reference the IRS opinion letter and include its serial number when completing the form, as this confirms the plan’s qualification. If you are filing Form 5500-EZ for the first time, you should check box A(1) on Part I of the form. You can file it by mail or electronically, depending on your total number of annual IRS filings. If you’re a solo business owner, Form 5500-EZ is likely your responsibility. And if no one is tracking it, you could be sitting on a six-figure mistake. What Is Form 5500-EZ?

2. Form 5500

Used by businesses with employee retirement plans. If you have full-time staff enrolled in a 401(k) or similar plan, this is likely your required filing. It must be submitted electronically through the Department of Labor’s EFAST2 system.

3. Form 5500-SF (Short Form)

For small businesses with fewer than 100 participants in the plan. This is still for employee plans, not solo owners, and requires electronic filing. Think of it as a streamlined version of the full 5500.

Plan Eligibility: Are You Required to File?

Wondering if Form 5500-EZ is on your to-do list? The answer depends on the structure of your retirement plan and your business. The Internal Revenue Service (IRS) requires annual reporting for one participant plans—these are retirement plans that cover only you (the business owner) or you and your spouse, whether your business is incorporated, unincorporated, or a business partnership. If your plan covers just the partners (and their spouses) in a partnership, you’re in the one participant category.

Unlike larger plans subject to ERISA, one participant plans are governed by the Internal Revenue Code, which imposes its own filing obligations. That means even if you don’t have any other employees, you’re still responsible for annual reporting to the IRS using Form 5500-EZ. This applies whether your plan is a solo 401(k), a defined benefit plan, a money purchase pension plan, or another qualified retirement plan set up for yourself or your partnership.

If you’re the plan sponsor or plan administrator for a one participant plan, it’s your job to file Form 5500-EZ each year you meet the filing requirements. Don’t assume your business structure or lack of employees exempts you—if you’re running a retirement plan for yourself or your partnership, the IRS expects you to file. Understanding these eligibility rules is the first step to staying compliant and avoiding costly surprises down the road.

What Is Form 5500-EZ?

Form 5500-EZ is an annual return used by one-participant plans and certain foreign plans to satisfy annual reporting obligations imposed by the Internal Revenue Code. It is an information-only return that must be filled out by 401(k) plan administrators. Filing Form 5500-EZ creates an official record of contributions, loans, rollovers received, and asset holdings for a Solo 401k plan, and starts the IRS’s three-year statute of limitations for audits. If a Solo 401k plan is terminated, Form 5500-EZ must be filed regardless of the asset amount. If you have a Solo 401k with over $250,000 in assets, the IRS requires you to file Form 5500-EZ each year. You must include the total value of all plan assets, including unrealized gains and rollovers received, when determining if you need to file Form 5500-EZ. You must enter your total plan assets at the beginning and end of the calendar year in Part III of Form 5500-EZ. If you have outstanding participant loans, you must check ‘Yes’ on question 9 in Part V of Form 5500-EZ. When calculating net plan assets, future distributions are not included in liabilities. Accurate participant information and plan information must be provided on the form.

5500 EZ is a simple two-page document. It tells the IRS that your plan exists, how much is in it, and confirms that you’re following the rules. Nothing wild. But if you don’t file it when required, the IRS charges $250 per day, up to $150,000 per missed return. And yes, that’s per plan, per year.

Get the form on the official IRS page:About Form 5500-EZ

Your P&L Is Hiding Growth.

We run your business against the 60-15-15 operating standard and show you exactly where the gaps are — plus your enterprise value and a custom tax strategy. Three meetings. One complete picture.

We take 15 per month.

When Must Form 5500-EZ Be Filed?

The $250,000 threshold for filing Form 5500-EZ is determined based on the total balance across all plan participants and every Solo 401k plan you have. If you have multiple Solo 401k plans, you must add the balances of all your accounts—including spouse accounts—to determine if you exceed the $250,000 threshold. If your Solo 401k plan had more than $250,000 in total assets during the previous calendar year, you must file Form 5500-EZ. For calendar-year plans, the Form 5500-EZ is due by July 31 of the following year. The filing deadline for Form 5500-EZ is the last day of the seventh month after the end of the plan year. You can request an extension of up to 2 ½ months for filing Form 5500-EZ by submitting Form 5558 before the original due date.

The moment your plan hits $250,000 in assets by the end of the plan year, you’re required to file it. Doesn’t matter how it got there—contributions, rollovers, or investment growth. If you close the plan or roll funds out, you owe a final return that says everything has been distributed. If last year was the final year of your Solo 401k, you must file Form 5500-EZ even if your total plan assets were less than $250,000. If your plan value is below $250,000 and you’re not officially closing your account, filing Form 5500-EZ isn’t mandatory, but it may still be a smart move.

That final return is where many owners get nailed. The account balance drops to zero. They assume they’re done. But that last filing is mandatory, and not filing it still triggers penalties.

If you have multiple solo plans and their combined balance passes $250,000, you now need to file one for each plan, even the ones under the threshold.

How to File the 5500-EZ: Electronic vs. Paper Submission

While Form 5500-EZ can be filed either electronically through the EFAST2 system or by mailing a paper copy to the IRS, electronic filing is generally recommended. Electronic submissions are processed more quickly and reduce the risk of lost or delayed mail. Starting in 2024, if you file multiple returns annually, you are subject to the electronic filing requirement and must file Form 5500-EZ electronically through the EFAST2 system. Form 5500-EZ, along with other forms such as 5500 and 5500-SF, are typically filed electronically using the DOL EFAST2 system. You may also need to include other forms or paperwork when submitting your filing, depending on your plan’s circumstances. For detailed procedures on filing, requesting extensions, and ensuring compliance, always consult the official IRS instructions.

What To Do If You Missed The Deadline

If the IRS hasn’t sent you a penalty notice yet, there’s still a shot. To avoid penalties, file as soon as possible and use the IRS Late Filer Penalty Relief Program if eligible. Submit your old forms, pay $500 per year (max $1,500 per plan), and the IRS lets you off the hook. If you realize you are delinquent in filing Form 5500-EZ, you can submit Form 14704 to reduce your penalty to $500 per year, up to a maximum of three years.

But once they issue the penalty, that option disappears.

The IRS allows for penalty relief if there is a valid reason for the late filing of Form 5500-EZ. Valid reasons include natural disasters, severe illness, or lack of access to records, but forgetting to file is not considered valid. At that point, your only hope is something called reasonable cause relief, and the bar for that is high. Fires, illness, incapacitation, missing records, etc. “I didn’t know” won’t cut it. And if your request gets denied, you’re back in penalty land with no second chance.

What This Really Tells You About Your Financial Strategy

This isn’t a filing issue. It’s a strategy issue.

You’ve got a retirement account with real money in it. That account has rules. Those rules aren’t flagged by TurboTax or your bookkeeper. And unless someone is actively managing the structure of your plan—thresholds, timelines, rollouts, final returns—you’re betting your tax savings against the IRS’s penalty system.

There’s nothing complicated about the 5500-EZ. But what it reveals is bigger: a lack of oversight, a lack of integration, and a lack of strategy.

Most business owners are exposed, and they don’t even know it.

If your financial team isn’t tracking this, what else are they missing? Learn more about fractional shares and their pros and risks.

Self-employed individuals should pay special attention to plan characteristics and codes when filing, especially if this is your first plan or you are restating an existing one. If your Solo 401k plan includes a participant-directed brokerage account or profit sharing, you must report these features using the appropriate codes. When valuing your plan, include all contributions, rollovers, and assets from other plans to ensure accurate reporting. Solo 401k plans do not have a minimum funding requirement, offering flexibility for self-employed individuals. Always consult a qualified tax advisor or legal counsel for guidance on compliance, plan setup, and filing requirements to avoid costly mistakes.

This is what we mean when we say strategy beats compliance. You don’t just need a plan. You need someone who understands what that plan touches, and what happens when it gets ignored.

Your cash should be compounding, not getting vaporized by missed forms.

Talk to our tax planning experts before a small oversight turns into a six-figure hit.

Ready to See Your Numbers?

The Scale-Ready Assessment is a full financial diagnostic for service businesses doing $1M–$20M. You’ll get your 60-15-15 scorecard, enterprise value gap, custom tax strategy, and a prioritized roadmap — all in three meetings.

$96.2M in client revenue under active management · 200+ companies analyzed

FAQs About Form 5500-EZ: The $150,000 Mistake Hiding in Your Retirement Plan

What Is Form 5500-EZ and Who Needs to File It?

Form 5500-EZ is the IRS filing required for one-participant retirement plans—like solo 401(k)s or owner-only defined benefit plans. It confirms your plan exists, reports assets, and ensures you’re following retirement regulations. Required for individuals or owner-spouse businesses with no employees. Applies once total plan assets exceed $250,000 at year-end. Also required when the plan terminates, even with a $0 balance. Learn how this fits into a broader tax planning strategy or get official filing details on the IRS Form 5500-EZ page.

When Is Form 5500-EZ Required for Solo 401(k)s?

You must file Form 5500-EZ when your plan assets exceed $250,000 at the end of the plan year—or anytime the plan is closed, regardless of balance. Include total contributions, rollovers, and investment growth. If you manage multiple solo plans, file one for each if their combined balance exceeds the threshold. Failing to file can trigger penalties up to $150,000 per missed year. See how Bennett Financials integrates compliance tracking into your CFO services or review compliance rules on the Department of Labor’s site.

How Do You File Form 5500-EZ—Paper or Electronically?

You can file Form 5500-EZ either by mail or electronically. However, e-filing through the EFAST2 system is recommended for faster, safer processing. If you file ten or more IRS forms annually, electronic filing is mandatory. Paper forms risk being delayed or lost, extending exposure to penalties. Keep confirmation records of submission for audit protection. Bennett Financials helps clients automate these filings through strategic finance systems. Learn more on our Strategic Finance page.

What Happens If You Miss the 5500-EZ Filing Deadline?

If you’ve missed a filing, act fast. The IRS Late Filer Penalty Relief Program can limit your penalty to $500 per year (maximum $1,500 per plan). Submit your missed forms under this program before the IRS contacts you. Once a penalty notice is issued, you lose eligibility for relief. If denied, your only option is “reasonable cause relief,” which is rarely granted. For help restoring compliance and minimizing fines, connect with our tax strategy team or review details directly on IRS.gov.

Why Do Most Business Owners Miss Form 5500-EZ?

Many owners assume their CPA or plan provider handles the filing—but most don’t track it automatically. The IRS doesn’t send reminders, and missing it can cost up to $150,000. Plan providers often manage contributions, not compliance filings. Bookkeepers and tax software rarely flag this obligation. Without oversight, a simple omission can become a six-figure penalty. Bennett Financials monitors regulatory filings as part of proactive tax planning and compliance management. For reference, see official filing instructions on IRS.gov.

What is Form 5500-EZ: The $150,000 Mistake Hiding in Your Retirement Plan about?

Got a solo 401(k)? Then the IRS is expecting a form from you. One you’ve probably never heard of. It’s called Form 5500-EZ. It’s short, easy to overlook, and skipping it can cost you up to $150,000 in penalties. Most business owners miss it. Their CPA doesn’t file it. Their plan provider doesn’t flag it. The IRS won’t remind you. But when they catch it, they charge you. If you’ve got money in a one-participant retirement plan and no one’s tracking this form, you’re exposed. Here’s what to do about it.

What should I know about The Three Types of Form 5500: Know Which One You Need?

Not all Form 5500 filings are the same. There are three variations, and choosing the wrong one or ignoring the one that applies to you can lead to compliance issues or steep penalties. If your business is a sole proprietorship, you may need to obtain a business EIN rather than using your SSN, as the IRS requires the correct identification for Solo 401(k) plan filings.

What should I know about 1. Form 5500-EZ?

Applies to one-participant retirement plans. This typically covers solo 401(k)s, which are a type of defined contribution plan offering flexibility in contributions and no minimum funding requirement, or owner-only defined benefit plans. If it’s just you or you and your spouse, this is the form you need. If you adopted a pre-approved plan, be sure to reference the IRS opinion letter and include its serial number when completing the form, as this confirms the plan’s qualification. If you are filing Form 5500-EZ for the first time, you should check box A(1) on Part I of the form. You can file it by mail or electronically, depending on your total number of annual IRS filings. If you’re a...