Form 8275: The IRS Form That Could Save You from a Six-Figure Penalty

Imagine bleeding six figures in cash over a single IRS penalty – money that should’ve stayed in your business, funding your next hire or growth push. For a $2–$20 million business, one tax mistake can tank a quarter’s worth of progress. And here’s the kicker: it’s often avoidable.

If your CPA or CFO isn’t talking to you about Form 8275, you’ve got a problem. This form exists for one reason – to protect you from penalties when you take a legitimate but aggressive tax position. The IRS requires what’s called adequate disclosure to mitigate penalties, as outlined in the Internal Revenue Code. And right now, most business owners are flying blind.

Here’s how to use this form to shield your cash flow, protect your downside, and stay aggressive with your tax strategy – without waking up to a surprise letter from the IRS.

What Is IRS Form 8275 (and Why It Matters)

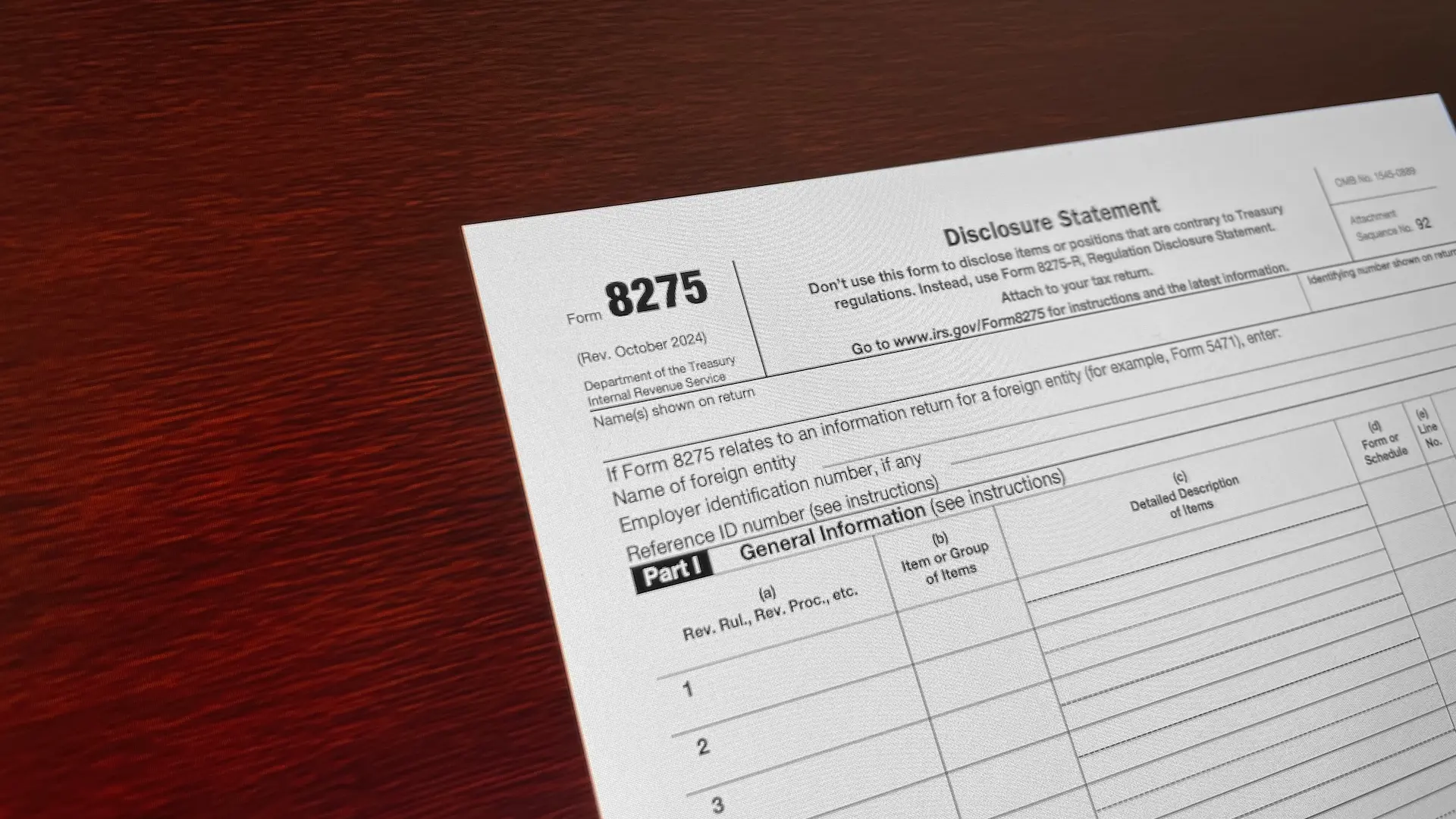

Form 8275, Disclosure Statement, is a tax disclosure form used by taxpayers and tax return preparers to disclose items or positions that are not otherwise adequately disclosed on a tax return. Form 8275 is used to make adequate disclosure of tax positions to the IRS, which is essential for penalty mitigation. It is a tool to protect you from penalties when you take a tax position that’s in a gray area – meaning there’s no “substantial authority” backing it up.

In plain English: you’re telling the IRS, “We took this position. Here’s why. We’re not hiding anything.”

That disclosure matters. Because if the IRS disagrees and you didn’t file Form 8275, you’re on the hook for back taxes plus a 20% penalty on the underpaid amount. Attaching a statement to the tax return ensures that relevant facts are adequately disclosed and can help avoid certain penalties. The IRS releases annual updates regarding adequate disclosure requirements to reduce penalties for taxpayers and tax preparers; the most recent update, Revenue Procedure 2024-44, outlines the appropriate use of Forms 8275 and 8275-R in various contexts.

For a $10M business with an aggressive $250K deduction that gets disallowed, that’s a $50K penalty for not having disclosed the item on a tax return to avoid accuracy-related penalties. That penalty doesn’t build your business. It doesn’t cover payroll. It’s just gone – because no one filed a two-page form.

A properly completed form 8275 must be filed with the original tax return to gain penalty protection for items not disclosed on a tax return.

What Happens If You Don’t Use It

Let’s be blunt: skipping Form 8275 when you should’ve filed it is reckless.

2.1 IRS Penalties: The $12K Mistake

If you take a position on your tax return that the IRS later disagrees with, you could owe an additional $12K in tax penalties. This is an accuracy-related penalty imposed for tax understatements when the understatement is attributable to items not adequately disclosed or due to unreasonable positions or disregard of rules.

2.2 Audit Risk: The Clock Keeps Ticking

Failing to disclose a questionable position can keep the audit window open for years. Substantial understatement of income or understatement of income tax can trigger certain penalties and extend audit periods.

2.3 CPA Liability: Not Just Your Problem

If your CPA or tax preparer doesn’t disclose a position that lacks substantial authority, they can be on the hook too. Tax return preparers can also face preparer penalties for failing to disclose unreasonable positions. Tax professionals can avoid preparer penalties for tax understatements due to unreasonable positions if Form 8275 is used properly.

2.4 Narrative Control: You Lose It

If you don’t disclose, you lose the chance to explain your reasoning up front. Proper disclosure, with a statement attached, provides penalty protection and helps avoid penalties for tax understatements.

Hefty Penalties That Drain Growth Capital

Say your company claims a $200K deduction that isn’t crystal clear. If the IRS disallows it and you failed to disclose, you’re not just paying the ~$60K in tax. You’ll owe an additional $12K penalty. That’s $12K in pure waste – money that could’ve funded new hires or equipment upgrades.

Interest Charges & Longer Audit Windows

It gets worse. You’ll also pay interest on the underpaid tax. And if the issue qualifies as a “substantial understatement,” the IRS can double the audit window – from 3 years to 6. That’s half a decade of uncertainty, hanging over your books.

CPA Liability & Relationship Fallout

If your CPA knew the position was aggressive and didn’t disclose it, they can get penalized too. That strains the relationship and often causes CPAs to go overly conservative on future returns – leaving tax savings on the table. Filing Form 8275 protects everyone.

You Lose Control of the Narrative

The IRS doesn’t care if your intent was good. If you didn’t disclose, you look like you were hiding something. That’s how you end up triggering deeper audits, penalties, and reputation risk.

When to Use Form 8275

Use Form 8275 any time you need to make disclosures relating to specific items, transactions, or reportable transactions—including non tax shelter items and reportable transactions—that are not fully detailed on the tax return. Form 8275 is used for gray-area positions lacking substantial authority but with a reasonable basis. Taxpayers, including individuals, corporations, and pass-through entities, use this form to disclose positions or transactions that may lack clear legal support, involve aggressive deductions or credits, involve unusual income classification, or could be questioned by the IRS, and maintaining proper bookkeeping to defend against IRS audits is a critical companion to these disclosures. Proper disclosure of the relevant facts affecting the item’s tax treatment can help mitigate penalties, including the economic substance penalty. Using Form 8275 can immunize taxpayers from accuracy-related penalties due to disregard of rules or substantial understatement of income tax for non-tax shelter items. Additionally, Form 8275 can eliminate exposure to a 40% penalty for transactions lacking in economic substance when properly completed.

Let’s break down a few real-world examples, keeping in mind that other international disclosure requirements like IRS Form 8858 for foreign disregarded entities can carry similarly steep penalties if ignored.

1. Gray-Area Deductions or Credits

Maybe you’re writing off a large software build under Section 174, or taking an R&D credit where eligibility is debatable. Disclose it. If the IRS later disagrees, you’ll pay the tax – but skip the 20% penalty when it’s paired with proactive, year-round advanced tax planning that anticipates these gray areas.

2. Unusual Income Treatments

Received a legal settlement and excluded it from income? Claimed a grant as non-taxable? If there’s any risk the IRS sees it differently, Form 8275 is your way of showing you had a reason – and weren’t trying to pull a fast one, especially when it’s grounded in tax planning that’s integrated with financial forecasting instead of last‑minute guesswork.

3. Strategic Entity Moves or Elections

Took a rare tax election? Structured a deal to optimize treatment? Claimed a home office deduction for a mixed-use space? If your CPA says “this could go either way,” that’s your signal to file—and major exits or asset sales may call for tools like a Deferred Sales Trust to defer capital gains tax alongside proper disclosure.

4. Pass-Through Entity Risks

If you’re in a partnership or S corp, and the entity takes a questionable position that flows to your return – file Form 8275 yourself and make sure your CFO‑level tax strategy and consultation process surfaces those issues before filing season. Ideally the entity files it, but you can protect your end with your own disclosure.

How to Use It Properly

1. File It with the Original Return

Do not wait to see if the IRS calls. Form 8275 needs to go in with the initial return. Most professional software allows it to be attached as a PDF for e-filed returns.

2. Be Clear and Concise

In Part II, explain what you did, the dollar amount involved, and the legal rationale, the same way you would document an advanced tax planning strategy for high‑net‑worth owners that needs clear support. Be sure to include key information: a description of the facts and legal issues, the amount, the affected form and line number, and the specific regulation or rule being challenged. Include references: IRS code sections, revenue procedures, relevant case law, court cases – whatever supports your position. Don’t write a novel. Just lay it out clean.

Example:

“Company deducted $50,000 in software dev costs as Section 174 expenses (Form 1120, Line 26). Position based on Rev. Proc. 2000-50, Tax Court decision in XYZ v. Comm’r, and supporting case law. Disclosure made to preserve reasonable basis protection.”

3. Use the Right Form

Use Form 8275 for positions not directly contradicting IRS regulations or Treasury regulations, and remember that other specialized filings such as Form 8858 for foreign disregarded entities and branches have their own disclosure rules and penalty structures. Form 8275 requires you to provide specific details about tax positions that are contrary to regulations or revenue rulings. If you’re taking a position that directly contradicts a Treasury regulation, you must use Form 8275-R, which serves as a regulation disclosure statement. Most of the time, the standard 8275 will do unless your position is contrary to Treasury regulations, in which case 8275-R is required.

4. File Multiple Forms if Needed

If you’ve got several questionable positions, use multiple forms – one per issue. Keeps the disclosures clean and focused.

5. Keep Your Backup

Form 8275 is a summary. Keep the full documentation ready to go: legal memos, emails, notes. If you get audited, you’ll need to prove you had a reasonable basis.

A Real Example: How One Business Saved $20K with a Single Form

A marketing agency treated a six-figure revenue item as a capital contribution due to the nature of the deal. The tax savings? $100K—exactly the kind of outcome that’s possible when an agency has specialized CFO and tax services for marketing firms guiding structure and disclosures.

The owner disclosed the position using Form 8275.

Two years later, the IRS challenged it. He owed the tax, plus interest – but no penalty. That’s a $20,000 win for two pages of paperwork.

If he hadn’t disclosed? That same tax savings would’ve cost him an extra $20K in penalties.

How to Use Form 8275 as a Strategic Advantage

1. Keep More of Your Cash, Safely

Sometimes the tax law is unclear. That doesn’t mean you shouldn’t pursue the savings – it means you should do it smart. Form 8275 lets you play offense without gambling with your cash flow when it’s part of broader strategic finance and fractional CFO services that manage risk across the whole business.

2. Maintain Good Standing with the IRS

Filing Form 8275 shows you’re not being shady. The IRS isn’t out to get you if you’re upfront. Full disclosure improves audit outcomes and keeps issues contained, especially when paired with audit‑ready books and documentation practices.

3. Contain the Scope of Audits

If you disclose, the IRS tends to focus on that item. If you don’t and they discover something? Expect them to start digging. One red flag turns into an audit fishing expedition. Disclosure protects your time and mental bandwidth.

4. Use It as a Planning Checkpoint

Ask your tax team every year: “Do we need any Form 8275s this year?” If the answer is always no, start questioning if you’re missing opportunities. This form should show up in real tax planning, not just compliance, and a year‑round CFO consultation model for tax strategy helps make that review automatic.

Link to download the official form: https://www.irs.gov/forms-pubs/about-form-8275

Bottom Line

Form 8275 is not about being clever. It’s about being strategic.

You don’t grow a company by overpaying tax and praying the IRS doesn’t notice a gray area. You grow by taking strong positions with protection in place. And this form gives you that protection.

However, Form 8275 cannot be used to avoid penalties for tax shelter items; for those, Form 8886 is required. For broader context on structuring your tax posture and operations, our elite tax and financial strategy articles dig into how different structures interact with IRS disclosure rules. Additionally, filing an amended return or a qualified amended return can be a strategic way to correct previously filed returns and potentially reduce penalties, especially when disclosing additional information or correcting inaccuracies, and it should fit within a larger framework of advanced, proactive tax planning for your business.

If your accountant isn’t using it – or doesn’t know how – then it’s time to upgrade your tax team to one that provides fractional CFO services with integrated tax planning and broader strategic finance support for growing companies.

Want to build a tax strategy that protects your downside while unlocking real savings?

We do this every day for high-growth businesses through a team that’s laser‑focused on strategic financial planning and tax optimization for entrepreneurs with clear, structured CFO and tax service packages. Book a consultation today.

FAQs About IRS Form 8275: The Disclosure Form That Can Save You from a Six-Figure Penalty

What Is IRS Form 8275 and Why Does It Matter?

IRS Form 8275, the Disclosure Statement, is designed to protect taxpayers from accuracy-related penalties when they take a position on their tax return that lacks clear “substantial authority.” In simple terms, this form tells the IRS: “We took this tax position, here’s our reasoning, and we’re being transparent.” Used when claiming legitimate but aggressive tax positions Prevents the 20% accuracy-related penalty under Section 6662 Applies to deductions, credits, or income treatments with gray-area interpretations To see how strategic disclosure protects your business, explore our Tax Planning services or review the official IRS Form 8275 instructions.

When Should a Business File Form 8275?

Form 8275 should be filed any time your company takes a position that could be challenged or questioned by the IRS. Common situations include: Large or complex deductions without clear authority Unusual income exclusions or expense classifications Tax credits with ambiguous qualification rules Entity restructuring or rare elections It’s especially valuable for businesses in growth phases that push into more complex financial strategies. To identify when your tax strategy needs disclosure, review your return with our Fractional CFO Services or explore guidance from Investopedia.

What Happens If You Don’t File Form 8275 When You Should?

Failing to file Form 8275 can cost your business tens—or even hundreds—of thousands in penalties. 20% accuracy-related penalty on underpaid taxes Interest on unpaid balances Possible audit extension from 3 to 6 years Damage to CPA-client relationship and audit credibility Disclosure prevents these outcomes by proving transparency and good faith. For penalty prevention strategies, visit our Tax Planning page or see the IRS penalty breakdown on IRS.gov.

What’s the Difference Between Form 8275 and Form 8275-R?

Both forms serve to disclose tax positions, but they’re used in different contexts: Form 8275: For tax positions not directly contradicting IRS regulations Form 8275-R: For positions that do contradict a regulation Most small- to mid-sized businesses use the standard 8275 for deductions, credits, or income treatment issues. Need help determining which version applies to your business? Our Tax Advisors can help clarify. You can also review the difference explained at Cornell Law School’s Tax Regulations.

How Do You File Form 8275 Correctly?

Proper filing is critical to receive penalty protection: Attach Form 8275 to your original return (not amended) Clearly describe the tax position, dollar amount, and rationale Reference supporting code sections, rulings, or court cases Use one form per issue if multiple positions exist Maintain backup documentation in case of audit This proactive filing shows good faith and strengthens your legal standing. Get step-by-step support through our Tax Planning team or review detailed IRS filing instructions on IRS.gov.

What is Form 8275: The IRS Form That Could Save You from a Six-Figure Penalty about?

Imagine bleeding six figures in cash over a single IRS penalty – money that should’ve stayed in your business, funding your next hire or growth push. For a $2–$20 million business, one tax mistake can tank a quarter’s worth of progress. And here’s the kicker: it’s often avoidable. If your CPA or CFO isn’t talking to you about Form 8275, you’ve got a problem. This form exists for one reason – to protect you from penalties when you take a legitimate but aggressive tax position . The IRS requires what’s called adequate disclosure to mitigate penalties, as outlined in the Internal Revenue Code. And right now, most business owners are flying blind. Here’s how to use this form to shield your...

What should I know about What Is IRS Form 8275 (and Why It Matters)?

Form 8275, Disclosure Statement, is a tax disclosure form used by taxpayers and tax return preparers to disclose items or positions that are not otherwise adequately disclosed on a tax return. Form 8275 is used to make adequate disclosure of tax positions to the IRS, which is essential for penalty mitigation. It is a tool to protect you from penalties when you take a tax position that’s in a gray area – meaning there’s no “substantial authority” backing it up.

What should I know about What Happens If You Don’t Use It?

Let’s be blunt: skipping Form 8275 when you should’ve filed it is reckless.